Jul, 15 2026

Jul, 15 2026

Picture this: you’ve been paying $15 every month for your generic blood pressure medication. It feels like a small price to pay. But when you look at your year-end statement, you realize those payments didn’t move the needle on your deductible at all. You’re still stuck in that expensive middle ground where you pay coinsurance for doctor visits, even though you’ve spent hundreds of dollars on prescriptions.

This confusion is incredibly common. For years, people assumed that any money leaving their pocket for healthcare counted toward meeting their deductible. The reality is more complex. Under current health insurance rules, particularly those shaped by the Affordable Care Act (ACA), generic copays usually count toward your out-of-pocket maximum, but they often do not count toward your deductible. Understanding this distinction can save you thousands of dollars and reduce significant stress during open enrollment or unexpected medical events.

The Core Difference: Deductible vs. Out-of-Pocket Maximum

To understand how your prescription bills are treated, we first need to separate two terms that most people use interchangeably. They are not the same thing, and confusing them leads to financial surprises.

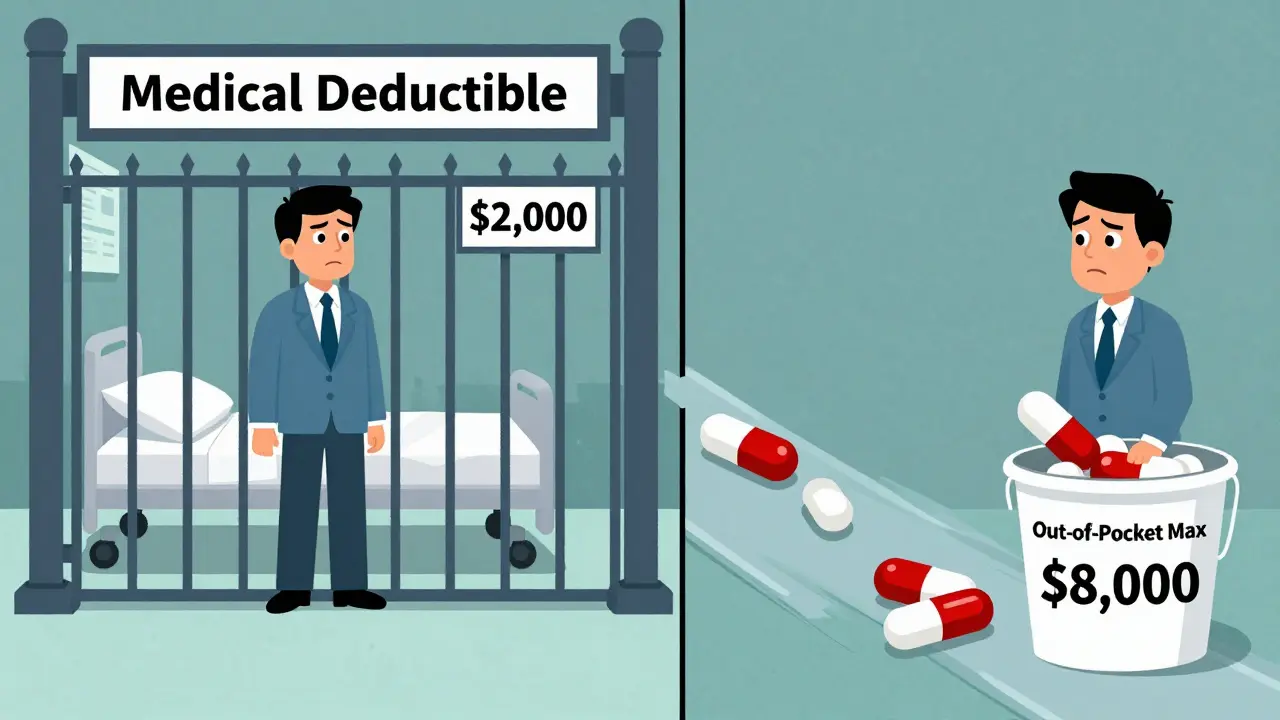

Your deductible is the amount you must pay out-of-pocket before your insurance starts sharing the cost of covered services. Think of it as a gatekeeper. If your deductible is $1,500, you pay the first $1,500 of eligible medical costs. After that, you might pay a percentage (coinsurance) while the insurer pays the rest.

Your out-of-pocket maximum is the absolute ceiling on what you will pay in a plan year for covered services. Once you hit this number, your insurance pays 100% of covered costs for the remainder of the year. This includes your deductible, coinsurance, and usually your copayments. It does not include your monthly premiums.

Here is the tricky part: payments count toward these buckets differently. In many plans, a $20 copay for a generic drug adds to your out-of-pocket maximum total but sits completely outside your deductible calculation. This means you could pay $1,000 in copays over the year, yet still owe the full $1,500 deductible if you need surgery.

| Payment Type | Counts Toward Deductible? | Counts Toward Out-of-Pocket Max? |

|---|---|---|

| Deductible Payments | Yes | Yes |

| Copays (Generic Drugs) | No (usually) | Yes |

| Coinsurance | Yes | Yes |

| Premiums | No | No |

Why Generic Copays Usually Don't Count Toward Deductibles

You might wonder why insurers structure plans this way. It comes down to how different types of coverage are priced. Generic drugs are considered low-risk, predictable expenses. Insurers negotiate fixed rates with pharmacies for these medications. Because the cost is known and stable, they often exempt these payments from the deductible to encourage patients to fill necessary prescriptions without worrying about hitting a high threshold first.

However, this creates a "two-track" system. Medical services (like X-rays or specialist visits) typically follow the deductible-then-coinsurance path. Prescription drugs, especially generics, often follow a flat copay path. Since the copay is a fixed fee agreed upon by the insurer and pharmacy, it doesn't contribute to the variable pool of money used to calculate whether you've met your medical deductible.

This separation was a major point of contention before the ACA. Prior to 2014, some plans didn't even count copays toward the out-of-pocket maximum. That meant you could pay thousands in copays and still face unlimited costs for other services. The ACA changed that rule, mandating that all in-network cost-sharing-including copays-must count toward the out-of-pocket maximum. But it left the deductible structure largely intact, allowing insurers to keep copays separate from the deductible calculation.

The Three Common Plan Structures

Not all plans handle this the same way. When reviewing your Summary of Benefits and Coverage (SBC), you’ll likely encounter one of three models. Knowing which one you have is crucial for budgeting.

- Single Combined Deductible: Both medical and prescription costs count toward one deductible. In this model, you rarely see fixed copays for generics until after the deductible is met. Instead, you pay the full price or a percentage until you hit the limit. This is simpler but can be expensive upfront if you need lots of meds early in the year.

- Separate Medical and Prescription Deductibles: This is common in employer-sponsored plans. You might have a $1,500 medical deductible and a $300 prescription deductible. Your generic copays only start applying after you meet the $300 prescription deductible. Until then, you pay the full negotiated price. These payments count toward your out-of-pocket max but not your medical deductible.

- Copay-Only Structure (No Prescription Deductible): Here, you pay a flat $10 or $15 for generics from day one. There is no deductible for prescriptions. These copays count toward your out-of-pocket maximum but never touch your medical deductible. This is popular because it provides immediate access to affordable meds, but it can leave you surprised if you need major medical care later in the year.

According to data from the Kaiser Family Foundation, about 37% of employer plans use separate deductibles, while 36% use copay-only structures for prescriptions. Only 27% use a single combined deductible. This means the majority of workers are navigating systems where their pill bottle payments don't help them meet their hospital bill thresholds.

Real-World Impact: A Case Study

Let’s look at a realistic scenario to see how this plays out. Meet Sarah, who has a plan with a $2,000 medical deductible, a $10 generic copay, and an $8,000 out-of-pocket maximum.

In January, Sarah starts a new medication for cholesterol. She pays $10 per month. By December, she has paid $120 in copays. She also had a minor injury requiring an ER visit in March, which cost her $1,800 after insurance adjustments. Her total out-of-pocket spending is $1,920 ($1,800 ER + $120 meds).

Has she met her deductible? No. The $120 in copays did not count toward the $2,000 medical deductible. Only the $1,800 ER visit did. So, if she needs another procedure in January of the next year (before the reset), she still owes the remaining $200 of her deductible plus any applicable coinsurance.

However, she is closer to her out-of-pocket maximum. All $1,920 counts toward that $8,000 cap. If she had a major surgery costing $10,000 later that year, she would only pay the difference between her current spend and the max, minus any coinsurance already applied. The key takeaway: copays protect you from catastrophic costs via the out-of-pocket max, but they don't accelerate your progress toward the deductible.

2026 Updates: What’s Changing?

If you are enrolling in a plan for 2026, pay attention to the new federal limits. The Department of Health and Human Services adjusts these caps annually. For 2026, the maximum out-of-pocket limit for Marketplace plans is $10,600 for an individual and $21,200 for a family. This is an increase from the 2025 limits of $9,200 and $18,400, respectively.

While the caps are rising, the structural confusion remains. However, there is a shift happening. The Centers for Medicare & Medicaid Services (CMS) is testing "Integrated Deductible" models in several states. In these pilot programs, prescription costs-including copays-count toward a single, unified deductible. Early results show a 28% increase in medication adherence among chronic disease patients, likely because the financial mechanics are easier to understand.

Industry analysts predict that by 2027, 60% of major insurers will offer at least one plan design where generic copays count toward the deductible. This responds to consumer demand for simplicity. But for now, most plans still keep them separate. Always check the "Does this payment count toward my deductible?" column in your SBC document. It’s a small detail that makes a huge difference.

How to Navigate Your Plan Documents

You don’t need to be an actuary to figure this out. Just follow these steps during open enrollment or when you get your new ID card:

- Find the Summary of Benefits and Coverage (SBC): This is a standardized four-page document required by the ACA. It compares your plan to others in simple language.

- Look for "Prescription Drug Deductible": If this line exists and has a dollar amount, you have a separate deductible for meds. If it says "None" or "$0," you likely have a copay-only structure.

- Check the "Copay" Section: See if it lists specific amounts for generic drugs. If it does, note whether the document says these apply "before deductible" or "after deductible."

- Call Member Services: If the paper isn’t clear, call the number on your card. Ask directly: "Do my generic prescription copays count toward my medical deductible?" Write down the answer and the representative’s name.

Don’t rely on assumptions. As Dr. Karen Pollitz from the Kaiser Family Foundation noted, the separation between deductibles and copayments creates a "valley of confusion" for consumers. Taking ten minutes to clarify this now can prevent frustration when you’re holding a bill later.

Frequently Asked Questions

Do generic copays count toward my out-of-pocket maximum?

Yes. Under the Affordable Care Act, all in-network cost-sharing, including generic prescription copays, must count toward your annual out-of-pocket maximum. Once you reach this limit, your insurance covers 100% of covered services for the rest of the plan year.

Why don't my copays count toward my deductible?

Many insurers design plans with separate tracks for medical services and prescriptions. Copays are fixed fees negotiated with pharmacies, so insurers often exclude them from the deductible calculation to keep premium costs lower. This means you pay the copay regardless of whether you've met your deductible, but the payment still helps you reach your out-of-pocket cap.

What is the out-of-pocket maximum for 2026?

For 2026 Marketplace plans, the federal out-of-pocket maximum is $10,600 for an individual and $21,200 for a family. Employer-sponsored plans may have different limits, but they cannot exceed these federal caps for non-grandfathered plans.

How can I tell if my plan has a separate prescription deductible?

Check your Summary of Benefits and Coverage (SBC). Look for a line item labeled "Prescription Drug Deductible." If it shows a dollar amount greater than zero, you have a separate deductible. If it says "None" or "$0," your plan likely uses a copay-only structure for prescriptions.

Will my copays count toward my deductible next year?

It depends on your plan design. While most current plans keep copays separate from deductibles, some insurers are testing "Integrated Deductible" models where all costs count toward one limit. Check your 2027 plan documents or ask your HR/benefits administrator if your employer is adopting this simpler structure.