Jul, 5 2026

Jul, 5 2026

Prescription drugs used to be a financial minefield for seniors. You’d pay your deductible, hit the "donut hole," and suddenly watch your costs skyrocket until you qualified for catastrophic coverage. That confusion is officially over. If you are looking at Medicare Part D, which is optional prescription drug coverage offered through private insurance companies approved by Medicare today, the rules have changed dramatically. The Inflation Reduction Act has rewritten the benefit design, capping what you pay out of pocket and simplifying how plans work.

For most patients in 2026, this means predictable costs. But predicting those costs requires understanding the new three-phase structure, the difference between plan types, and when you actually need to sign up. Let’s break down exactly how your medication costs are calculated now, so you can stop guessing and start saving.

How the New Three-Phase Structure Works

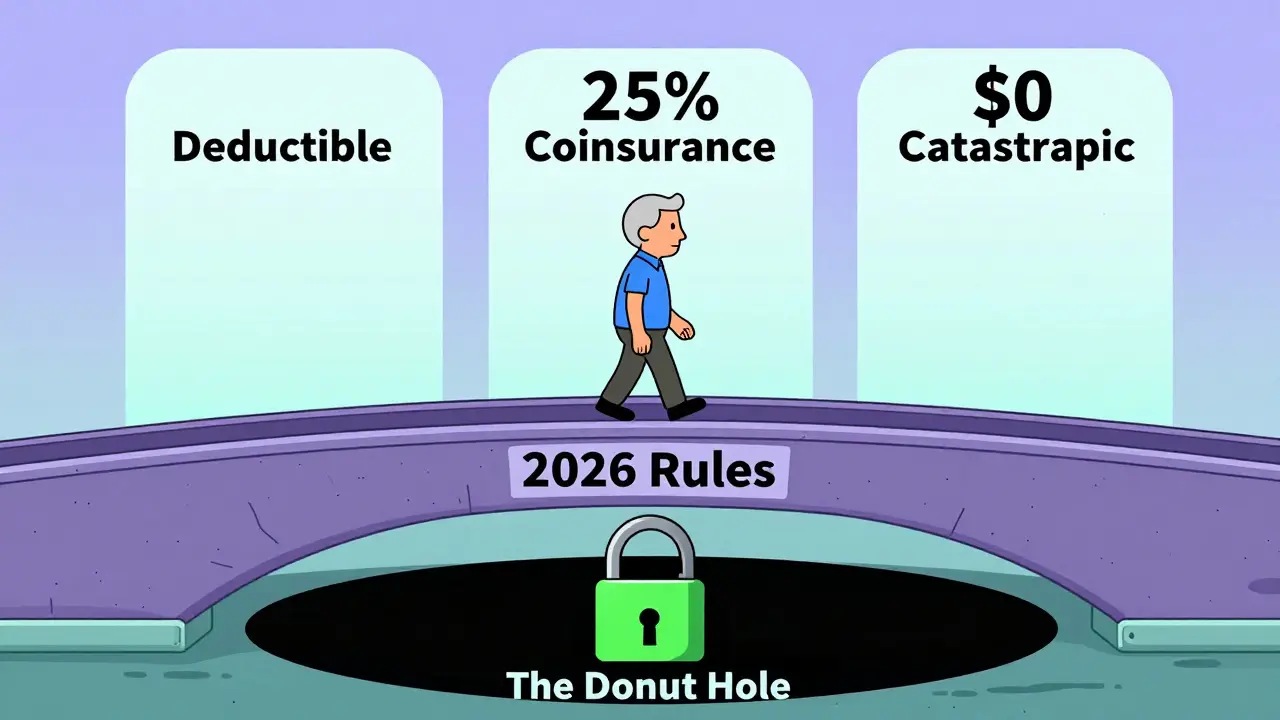

Gone are the days of tracking four different phases and worrying about falling into a coverage gap. Under the current design, implemented fully by the Centers for Medicare & Medicaid Services (CMS), your year is divided into three clear stages based on how much you spend on covered drugs.

- The Deductible Phase: At the start of the year, you pay 100% of your drug costs until you reach the annual deductible. For 2025, this maximum was $590. In 2026, expect this number to adjust slightly with inflation, but it remains a relatively low barrier to entry compared to past years.

- The Initial Coverage Phase: Once you pass the deductible, you enter the main coverage period. Here, you typically pay 25% coinsurance (or a flat copay) for your medications. The plan pays the rest. This continues until your total out-of-pocket spending hits the hard cap.

- The Catastrophic Coverage Phase: This is the game-changer. Once you have paid $2,000 out of pocket (in 2025 terms; rising to $2,100 in 2026), you enter catastrophic coverage. From that point forward, you pay nothing for covered drugs for the rest of the calendar year. No more 5% coinsurance. No more surprise bills.

This shift eliminates the infamous "donut hole." Previously, beneficiaries faced a gap where they paid significantly higher percentages of drug costs after initial coverage ended. Now, the transition from paying 25% to paying 0% is smooth and automatic once you hit that threshold. According to industry analysts at Avalere Health, this redesign reduces average out-of-pocket spending for beneficiaries by approximately 40% compared to previous projections.

Understanding Your Monthly Premiums

While your out-of-pocket costs for drugs are capped, your monthly premium is not. This is where many people get tripped up. The premium is the fee you pay every month to keep the plan active, regardless of whether you fill a single prescription.

| Plan Type | Average Monthly Premium | Best For |

|---|---|---|

| Stand-Alone PDP | $45 | Those with Original Medicare (Parts A & B) seeking flexible pharmacy choices |

| Medicare Advantage (MA-PD) | $7 | Those wanting bundled medical and drug coverage, often with lower upfront costs |

| Benchmark Plans (Low-Income Subsidy) | $0 | Eligible beneficiaries receiving Extra Help |

As noted by Kaiser Family Foundation (KFF) research, there is a massive disparity in premiums depending on how you enroll. Stand-alone Prescription Drug Plans (PDPs) average around $45 a month, while Medicare Advantage plans with drug coverage (MA-PDs) average just $7. Why the difference? MA-PDs are often subsidized by states or designed to attract members with lower premiums to offset higher medical utilization later. However, remember that a $0 or low-premium plan might have higher copays per pill. Always calculate the total annual cost: (Premium x 12) + Estimated Copays.

Formularies and Tiers: The Hidden Cost Drivers

Even with a $2,000 cap, not all drugs cost the same before you hit that limit. Every Part D plan has a formulary, which is a list of covered drugs organized into tiers. Your specific medication’s tier determines your copay amount during the initial coverage phase.

- Tier 1: Preferred generics. Usually the cheapest option, often $4-$10 per month.

- Tier 2: Non-preferred generics. Slightly higher cost than Tier 1.

- Tier 3: Preferred brand-name drugs. Moderate cost-sharing.

- Tier 4: Non-preferred brand-name drugs. Higher cost-sharing.

- Tier 5: Specialty drugs. These are high-cost medications for complex conditions like cancer or rheumatoid arthritis. Copays here can be significant until you reach the catastrophic cap.

If your doctor prescribes a specialty drug, check if it’s on Tier 4 or 5. A $2,000 cap sounds great, but if you’re paying $400 a month for a specialty med, you’ll hit that cap in five months. If you’re on generic blood pressure meds, you might never come close to the cap. This variability is why comparing plans annually is non-negotiable.

Enrollment Windows: When You Can Sign Up

You cannot join a Part D plan whenever you want. Missing these windows can result in a permanent penalty added to your monthly premium for as long as you have Part D coverage.

Your Initial Enrollment Period lasts seven months, starting three months before the month you turn 65, including your birthday month, and ending three months after. If you miss this window and do not have "creditable coverage" (drug coverage from an employer or union that is at least as good as Part D), you face a late enrollment penalty. This penalty is calculated as 1% of the national base beneficiary premium for each full month you were without coverage.

For existing beneficiaries, the Annual Enrollment Period runs from October 15 to December 7 every year. This is your chance to switch plans, drop Part D, or join for the first time if you missed your initial window. Changes made during this period take effect on January 1 of the following year. There is also a Shorter Enrollment Period (January 1 - March 31) if you need to switch from a stand-alone PDP to a Medicare Advantage plan, or vice versa, but only once.

Special Savings: Insulin and Extra Help

Two specific provisions offer targeted relief for certain patients. First, the insulin cap remains unchanged and robust. In 2026, Medicare Part D plans must cap the monthly cost of covered insulin products at $35. This applies regardless of the tier the insulin falls into, providing stability for diabetics who rely on daily medication.

Second, if your income is limited, you may qualify for the Extra Help program, officially known as the Low-Income Subsidy (LIS). If you qualify, your premiums drop significantly-often to $0-and your copays decrease. In 2025, 90 stand-alone plans were available with $0 premiums for those receiving this subsidy. You do not always need to apply separately; if you receive Social Security Disability Insurance (SSDI) or Supplemental Security Income (SSI), you may be automatically enrolled. Check your eligibility via the Social Security Administration website.

Common Mistakes Patients Make

Despite the simplified structure, confusion persists. Based on discussions in patient communities like r/medicare and surveys by the Medicare Rights Center, here are the most frequent errors:

- Ignoring the Premium vs. Copay Trade-off: Choosing the cheapest premium plan ($7) without realizing your specific drug has a $50 copay, whereas a $45 premium plan offers that same drug for $10. Over a year, the expensive copay plan costs more.

- Assuming All Pharmacies Are In-Network: Part D plans use specific pharmacy networks. Using an out-of-network pharmacy can mean paying full price, which does not count toward your $2,000 out-of-pocket cap.

- Not Updating Medication Lists: Formularies change every year. A drug covered last year might move to a higher tier or require prior authorization this year. Always verify your current prescriptions during Open Enrollment.

- Thinking the Cap Includes Premiums: The $2,000 (2025) / $2,100 (2026) cap applies only to out-of-pocket costs for drugs (deductibles, copays, coinsurance). It does not include your monthly premium payments.

Next Steps for Patients

To ensure you are getting the best deal in 2026, gather your current medication list, including dosages and frequencies. Use the official Medicare Plan Finder tool on Medicare.gov to input these details. Compare the total estimated annual cost, not just the monthly premium. If you have questions, call 1-800-MEDICARE or contact your State Health Insurance Assistance Program (SHIP) for free, unbiased counseling. Don’t wait until December; start reviewing your options in November to avoid the rush and ensure you understand the changes affecting your wallet.

What happens if I go over the $2,000 out-of-pocket cap?

Once you reach the out-of-pocket threshold (which is $2,100 in 2026), you enter the catastrophic coverage phase. In this phase, you pay $0 for all covered prescription drugs for the remainder of the calendar year. The plan, manufacturers, and CMS cover the remaining costs.

Does the out-of-pocket cap include my monthly premium?

No. The out-of-pocket cap only includes amounts you pay directly for medications, such as deductibles, copayments, and coinsurance. Your monthly premium is separate and continues to be charged regardless of your usage or out-of-pocket status.

When is the best time to change my Medicare Part D plan?

The primary window is the Annual Enrollment Period, which runs from October 15 to December 7 each year. Changes made during this time take effect on January 1. There are also special enrollment periods if you move, lose other creditable coverage, or qualify for Extra Help.

Is there a penalty for enrolling in Part D late?

Yes, unless you had creditable coverage from another source (like an employer). The penalty is 1% of the national base beneficiary premium for each full month you were eligible but did not enroll. This penalty is added to your monthly premium for as long as you have Part D coverage.

How much does insulin cost under Medicare Part D in 2026?

Under the Inflation Reduction Act, the monthly cost for covered insulin products is capped at $35. This cap applies to both preferred and non-preferred insulin brands, ensuring affordability for diabetic patients.